For every Yin, there is a Yang.

For every asset where sentiment is becoming extremely bullish, there is usually another where sentiment is becoming extremely bearish.

Right now, it is very obvious where investor bullishness resides: anything Tech, anything AI, or anything with a plausible link to it — Copper included.

But what sits on the other side of that trade?

Where is sentiment becoming as historically bearish as it is becoming historically bullish in Tech?

The short answer is: Industrials, Value and Europe.

The even shorter answer is: Cyclicals.

The Tech trade has already run a long way and is starting to look extended from a sentiment perspective.

It is tempting to say that, for the rally to continue, the market needs to broaden out.

That may be too strong.

A more realistic statement is that it would be healthy for the rally to broaden out.

And if the market does broaden, the most interesting opportunity may not be in the assets everyone already loves.

It may be in the assets investors have largely left behind.

The most contrarian position at the moment is to go long the broadening-out trade — and go long Cyclicals, especially Industrials, Europe and Value.

What’s in

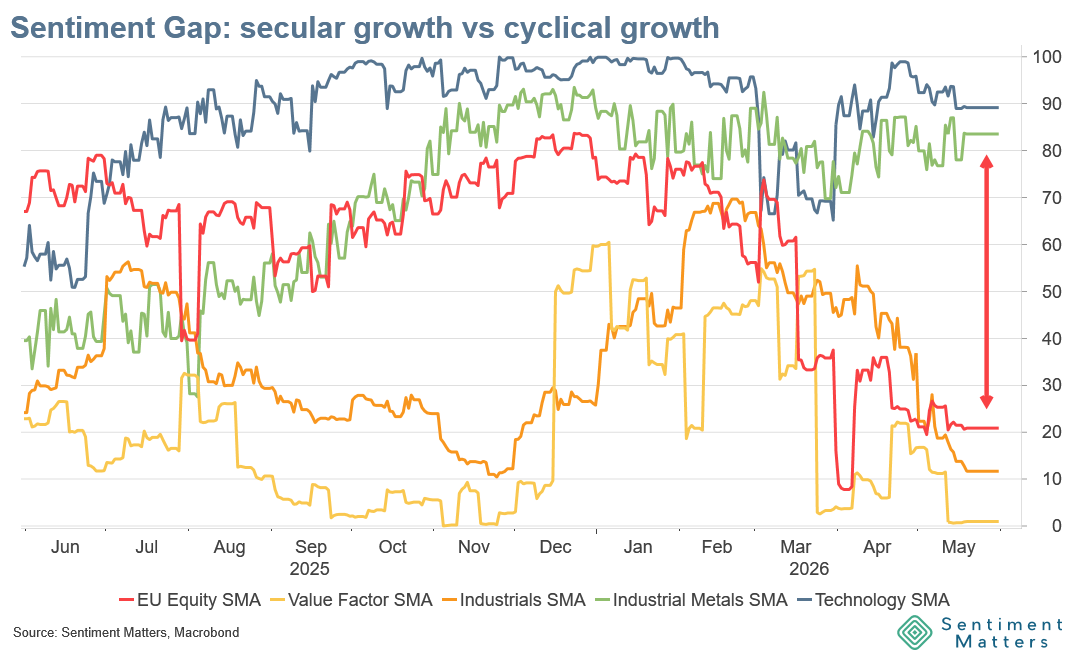

The recent rebound has been led by secular growth, not cyclical growth.

In practice, that means Tech has outperformed while Cyclicals have lagged.

That pattern says something important about the current market setup. Investors have become more confident that a recession can be avoided, but they are still unconvinced that the global cycle is about to re-accelerate.

The market is no longer pricing outright macro stress. But it is not fully embracing a broad-based recovery either.

That hesitation is understandable. Oil prices remain elevated, geopolitical risk has not disappeared, and there is still uncertainty around potential supply-chain disruption.

But it also means investors are returning to a familiar setup.

This is how much of 2025 played out. Secular, AI-driven growth in Tech looked more attractive than the weaker, more uneven growth available elsewhere in the market. Tech was the cleaner story. Cyclicals were more complicated.

In a K-shaped economy, investors crowded into the part of the market that could deliver growth without much help from the cycle.

That is where Tech’s scarcity premium comes from.

When growth is scarce, investors pay more for companies that can grow without much help from the economy.

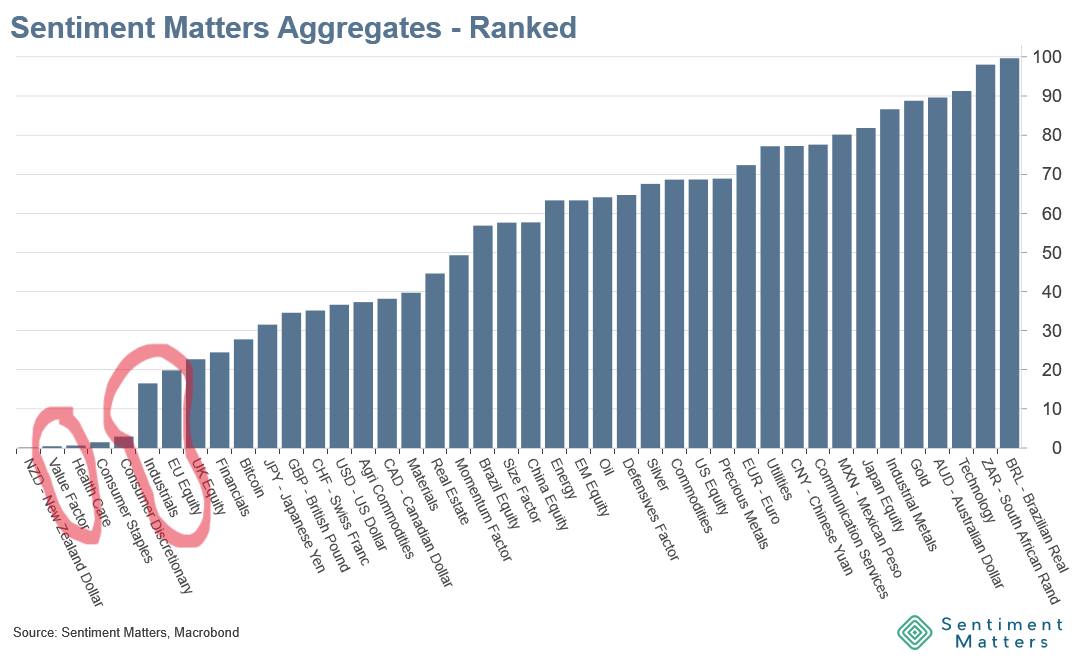

And that is reflected in the extreme bullishness we now register across the AI ecosystem. Technology is the asset with the third most bullish sentiment across all the assets we track. Communication Services and Copper are not far behind.

What’s out

Let’s look more closely at the parts of the market that now sit at the opposite sentiment extreme — the areas that have been left behind, but would stand to benefit if leadership broadens out again.

Our ranking of Sentiment Matters Aggregates is the best place to start when looking for the Yang to Tech’s Yin.

Value, Industrials and European equities are all among the seven least popular assets in our universe.