One of the biggest debates in markets right now is whether the equity market rally is a sign of rational market behaviour — or irrational complacency by equity investors.

Having spent years as an equity strategist on a fixed-income-dominated investment floor, I feel like I have had this debate many times before.

Déjà vu?

Here are my thoughts, from the perspective of a former equity strategist and current sentiment strategist.

Normal behaviour after a geopolitical shock

In many ways, this has been a textbook market response to a geopolitical shock.

The initial reaction was fast and emotional. Risk premia expanded across assets.

And then, just as quickly, much of that move reversed.

That pattern is not unusual.

Geopolitical shocks tend to create short-term dislocations. But those moves rarely persist unless the shock escalates and turns into a meaningful hit to global profits.

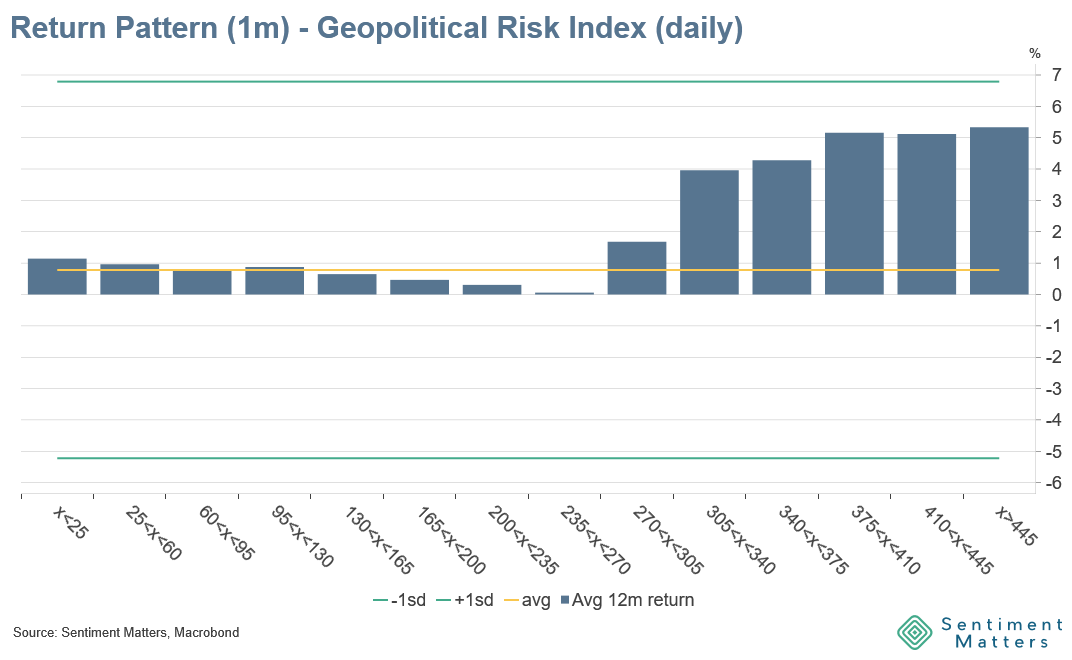

You can see this clearly in the Geopolitical Risk Index, which captures spikes in perceived geopolitical stress. Historically, those spikes have been followed by strong equity returns over short horizons. When the GPR moved above 300, the S&P 500 delivered above-average returns 81% of the time over the next month.

Bottom line: The equity rally is in line with the historical norm. Geopolitical shocks are usually short-term stress events and equity markets recover quickly.

Uncertainty falls faster than the conflict ends

Equity markets reflect the present value of expected future cash flows. There is no moral judgement involved.

A war matters for equity prices only to the extent that it changes future cash flows — or changes what investors are willing to pay for those cash flows today.

Wars and geopolitical shocks usually inject uncertainty into that process. That lowers equity prices.

On day one of a war, we know very little about the conflict and its potential consequences for corporate profits. The range of outcomes is enormous. Anything from “no meaningful impact” to “global recession” feels possible.

But then the research machine starts.

Geopolitical analysts write deep dives. Economists run scenarios. Bottom-up analysts quantify the potential impact on individual companies. Industry experts are brought in to explain supply-chain risks. Buy-side analysts map the exposures inside their funds. Every transmission mechanism is dissected.