31 July 2025

Bottom lines

- New Survey: Global institutions are bullish equities and private credit, bearish real estate

- Hedge fund betas say it all: neutral, cautious, and far from conviction

- US consumer surveys with contradicting messages: one bullish, one bearish. Who’s right?

- Big bullish shift from newsletter writers (II Bull-Bear)—but no sell signal yet

- Rising put/call ratios suggest caution—but not bearishness

- And the Biggest Bullish/Bearish Movers

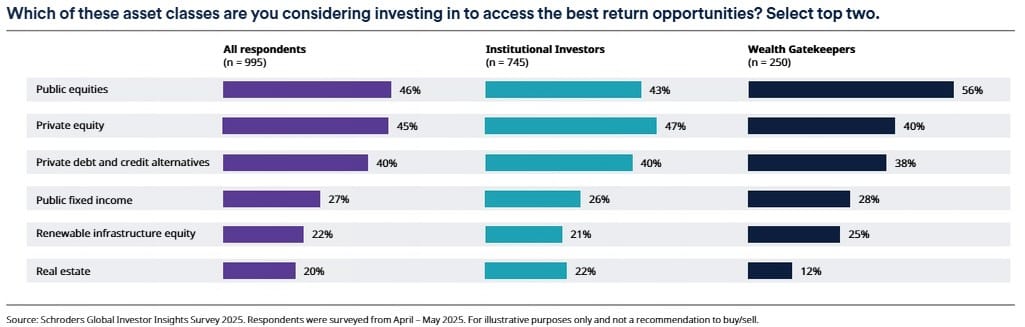

1) Schroders Global Investor Insights Survey

- Survey of 995 global investors (mostly institutional), conducted in April–May, after Liberation Day

- That makes its results somewhat stale tactically, but it still offers insight into positioning mindset

- Biggest macro concern (after tariffs): China–Taiwan tensions

- Nearly 1 in 4 expect volatility greater than during Covid or the GFC—a surprisingly high level of concern

- Despite this, equities are the most favoured asset class, and real estate the least

- “Wealth gatekeepers” (likely closer to retail) were more bullish than institutional respondents. This matches other surveys.

- Concentration risk is a very consensus concern (94%)—possibly amplified by US market underperformance post-Liberation Day

- Private credit is universally loved, as it is in every survey

- Decarbonisation is still a popular theme—86% plan to allocate more to it, but preferences have shifted:

- Hydrogen is going through the hype cycle. It has become the least popular decarbonisation area, after being extremely popular a few years ago

- Renewables are top-ranked, with nuclear in the middle