I don’t know about you, but I can’t forecast geopolitics. That’s exactly why I fall back on sentiment analysis.

The historical baseline is clear: geopolitical risk premia tend to mean-revert relatively quickly. The initial shock can be violent, but unless the situation escalates materially, markets usually adapt faster than the headlines do.

On the geopolitical side, we got the “buy the risk premium” signal almost immediately. The Geopolitical Risk Index (GPR) spiked to 565 — miles above the historical buy threshold at 300 — and it has stayed above 300 on most days since the war began. But the pattern is also familiar: unless there’s escalation, people adapt. Even a bad situation becomes the new normal and the GPR tends to drift lower over time. Ukraine is a good recent example.

Market stress, by contrast, has been building more slowly. A lot of indicators have shifted in a bearish direction, but it’s still hard to argue sentiment is extremely bearish. My best guess is we’d need another high-volume, big down day to push a broader set of risk-on/risk-off indicators into clear investor bearishness.

If we assume we cannot reliably trade every market lurch driven by one man’s tweets, then the more useful exercise is to look at where sentiment has shifted the most since the start of the war. That is usually where the most interesting opportunities lie once the geopolitical noise starts to fade.

This note is not about predicting the next headline.

It is about being ready for what comes after it.

Prepare, don’t predict. Do the homework now, while markets and sentiment are being pushed around by geopolitics, so you can respond faster when the next stage begins.

There are different ways to approach this question. We run through them below.

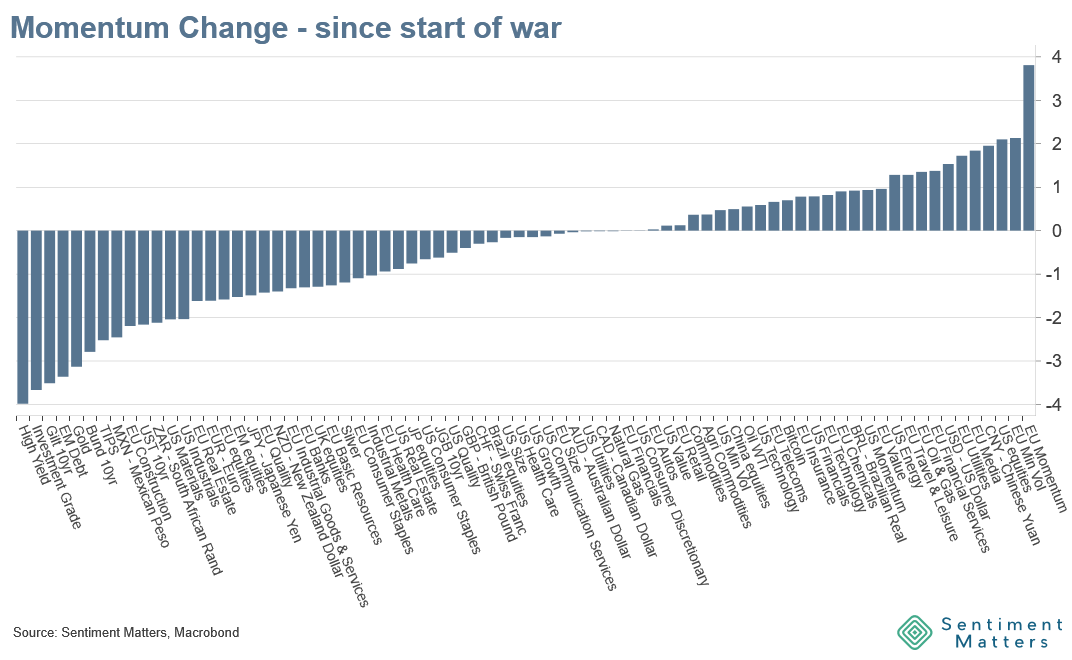

Where have prices adjusted the most?

The simplest screen is to look at where prices have moved the most — in either direction.

It’s a reasonable assumption that the war with Iran has been the dominant driver of most asset price moves over the past few weeks.

So, when the geopolitical risk premium mean-reverts and that driver fades, the price response will likely look like something like the inverse of what we have seen recently.

- The worst performers → potential buy-the-dip candidates

- The best performers → potential sources of funds

We show the change in our momentum score since the start of the war.