May 2026

Views from 48 top asset managers across 73 assets, based on 1,300+ individual views

Get all Buy Side Sentiment Tracker charts in a single presentation in the Toolbox section!

Main takeaways

- No buy-side euphoria

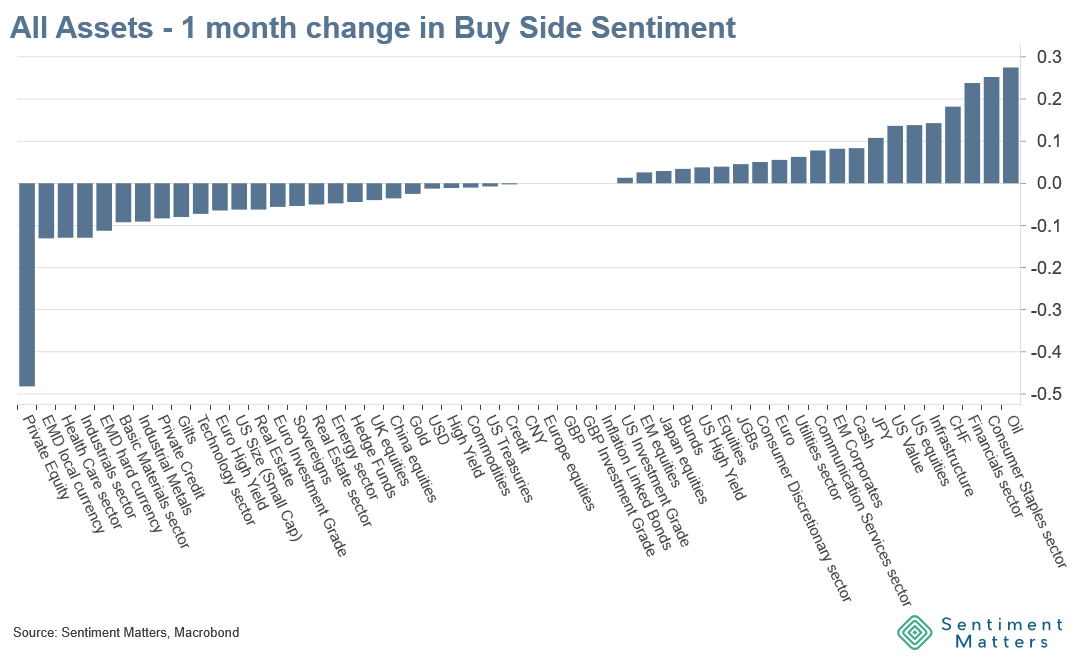

Despite the equity rally, there is still no sign of euphoria on the buy side. Overall sentiment remains cautiously optimistic at best — and still well below the levels seen before the Iran war. - Cyclicals are being cut

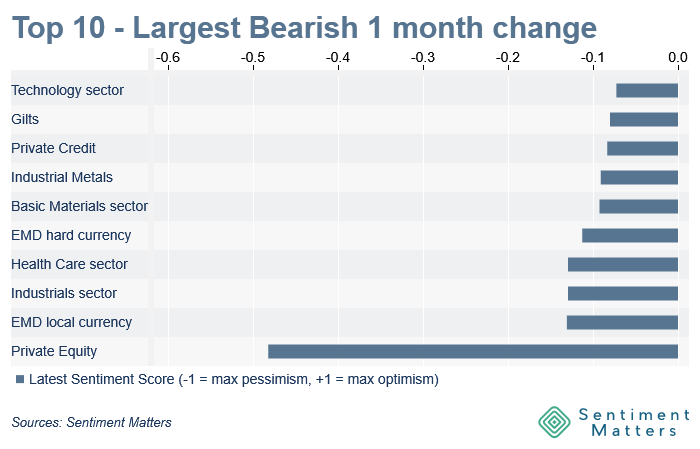

The clearest cross-asset message this month was another reduction in cyclical exposure. That is now the second month in a row. Investors are for economic disappointment. - The UK under pressure

Politics taking a toll? GBP is now the asset with the most bearish buy-side views in our tracker. Gilts were also downgraded, although they remain relatively popular given their high yield.

Sentiment: not as bullish as you might think

Buy-side sentiment fell despite the equity market rally.

Many investors remain sceptical about the sustainability of the rebound. That is consistent with the rally itself: sentiment has been as concentrated in pockets of the market as performance has been.

Risk appetite

- The risk appetite message was mixed, but with an overall bearish tilt.

- Risk appetite fell in 3 out of our 5 risk-on/risk-off indicators. Our aggregate risk-on/risk-off indicator is now at its lowest level since September. That is still close to the 2-year average and well above the post-Liberation Day low, but it is a clear cooling in buy-side enthusiasm.

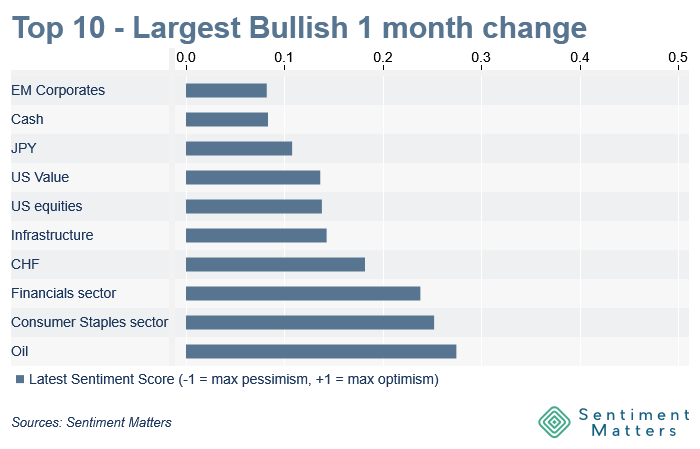

- Equities saw small upgrades to +56% net bullish. That makes them the most popular major asset class, but bullishness remains well below the +76% highs seen in February and March.

- There were a few upgrades on the month, but also one downgrade to underweight.

- 28 Bulls | 17 Neutrals | 1 Bear