April 2026

Views from 45 top asset managers across 73 assets, based on 1,300+ individual views

Get all Buy Side Sentiment Tracker charts in a single presentation in the Toolbox section!

Main takeaways

- Overall sentiment: the buy side has shifted toward neutral — not bearish. This looks like waiting out geopolitical stress, not a structural change in views.

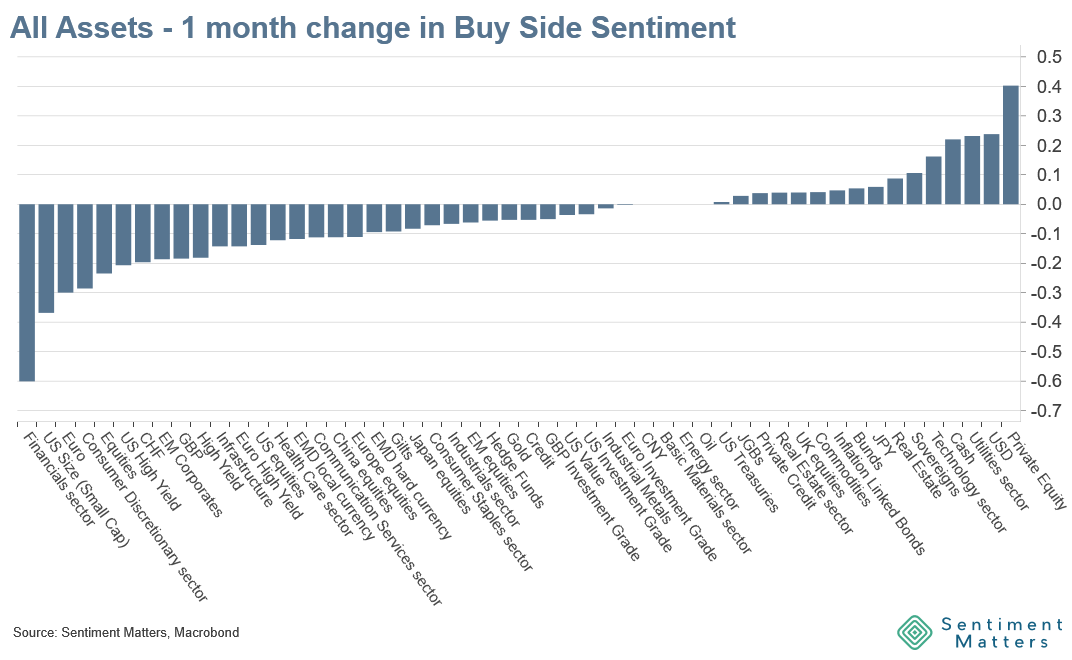

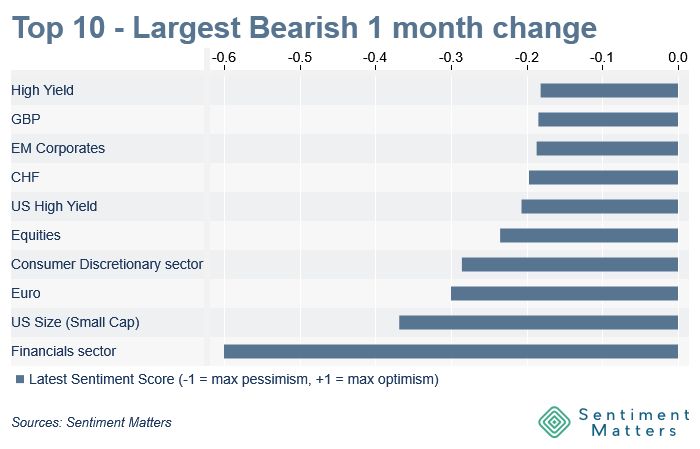

- Cyclicals: the clearest cross-asset message was cutting cyclical exposure — visible in regions, sectors, factors, and fixed income.

- Consumers down and out: Staples and Discretionary are now the two least popular sectors. Discretionary, however, is showing signs of resilience despite bad news. An interesting contrarian signal.

Sentiment: neutral, not bearish

Buy-side sentiment fell (unsurprisingly), but less than during last year’s tariff sell-off — and there are no signs of capitulation.

Risk appetite

- Risk appetite fell in all 6 risk-on/risk-off indicators.

- Our aggregate risk-on/risk-off indicator is back to November’s level: the lowest in 5 months, but still above average.

Major asset classes

- Equities: biggest drop in a year, but still +54% net bullish (still the 2nd most bullish major asset class).

- A lot of downgrades moved investors to neutral, but no downgrades to underweight.

- 23 Bulls | 21 Neutrals | 0 Bears

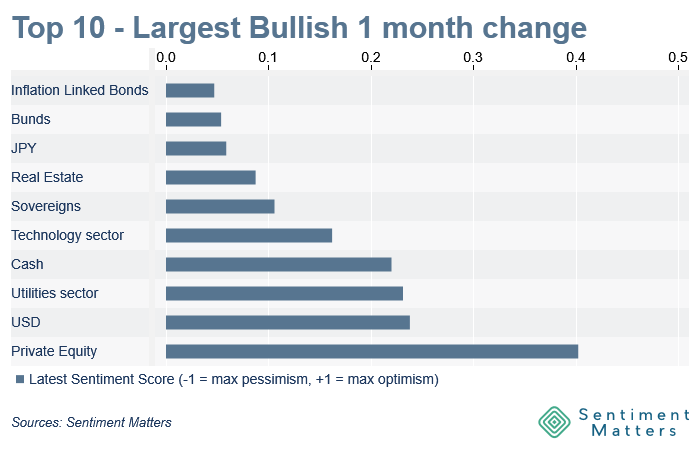

- Cash: biggest upgrade among major asset classes. Most popular since September, but still net bearish (still -21% underweight).

- Sovereigns: upgraded despite poor performance during the war — but only a small upgrade in a longer-term context. Still more Bears than Bulls.

- High Yield: among the Top 10 largest downgrades this month → lowest allocation since May 2025.