On my travels through Germany I visited an old friend in Wilhelmshaven last week. So, I had to visit the region’s latest attraction (see selfie), the new floating LNG terminal that played an important role in avoiding last winter’s energy crisis. Remember when we all worried about running out of gas? What better time to update my German gas model than a hot July day?

Supply

The supply side of the gas equation has not really changed much. There is still zero gas from Russia. But gas imports from other countries have been stable-ish and the LNG supply has come online roughly as expected.

Demand

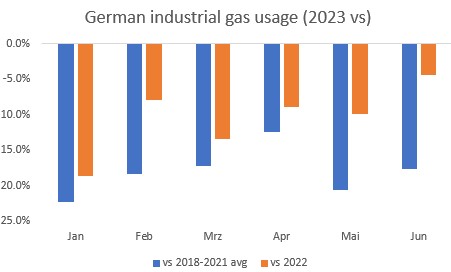

The positive surprise has been that gas demand has not increased with lower prices. The substitution away from gas has stuck. Some substitution decisions are difficult to reverse quickly, but risk aversion and changed habits are also likely playing a role. In some ways this is the new normal. German gas consumption has continued to run ~25% below the 2018-2021 average, with a lot of the difference coming from industry rather than households.

Source: Lars Kreckel, Bundesnetzagentur

Storage

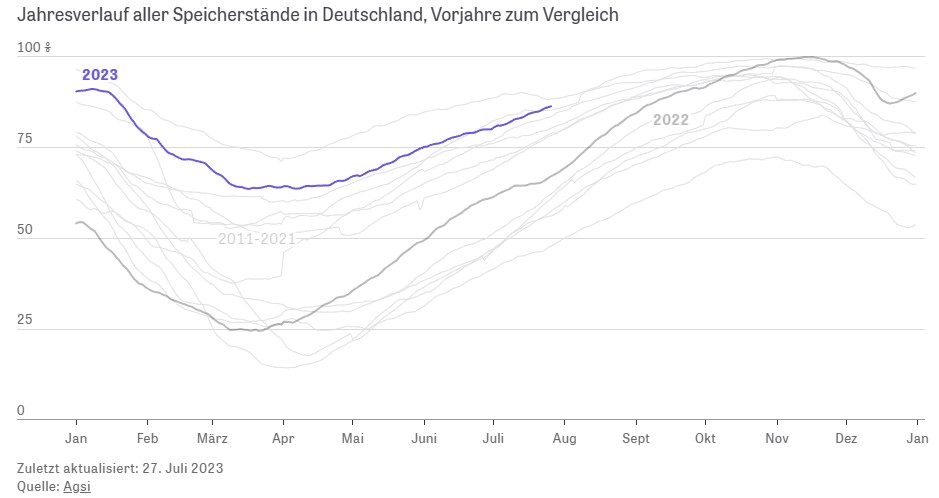

As a result, gas storage is filling up nicely. Having troughed at a surprisingly high 65%, storage levels have been rising since May and currently stand at 85.8%, just below the highest level at this time of year in recent history. That puts the goal of full storage well within sight before the weather turns colder. At the recent pace, storage would be at 100% in the middle of September.

Chart: German gas storage

Source: Zeit Energiepreismonitor

Outlook

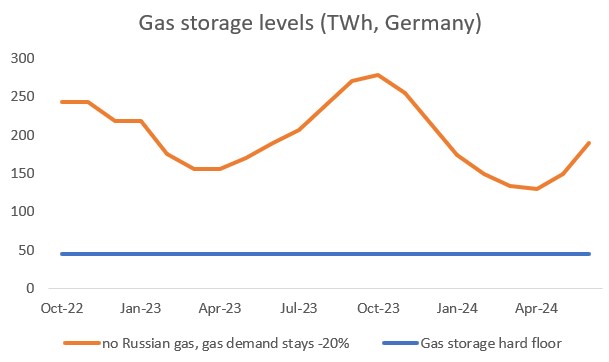

This paints a pretty relaxed picture for the next winter: full storage earlier than normal, sustainably reduced gas demand and further LNG capacity expected to come online in H2 and early next year. Assuming average seasonality this should mean storage levels trough just above half full next winter. The most vulnerable part of this equation is gas demand, but it would take a sudden and huge swing back towards falling in love with gas to threaten energy security. The other uncertainty is, of course, the weather. But overall, there should be a significant buffer against a cold winter in the system.

Source: Lars Kreckel

Bottom line: No replay of last winter’s energy crisis

Thanks for reading Macro Equity! Subscribe for free to receive new posts and support my work.